What Securitize's Tokenized Stock Launch Really Reveals

Learn the security tradeoffs between Solana and Avalanche for tokenized assets, and the key questions founders should ask before launching.

On the morning of July 2, 2026, a bell rang on the floor of the New York Stock Exchange, and Securitize became a publicly traded company under the ticker SECZ. That part of the story is ordinary. Companies list on the NYSE every week. What happened in the same few hours, on two blockchains that have nothing to do with Wall Street, is the part worth actually paying attention to.

Within that first trading session, Securitize tokenized roughly $295 million of its own newly listed common stock and made it available on Solana and Avalanche. Not a synthetic wrapper. Not a derivative product built by some unrelated exchange. According to CoinDesk, the tokens represent the same shares trading on the NYSE, issued directly by the company that just listed them, to investors who had already cleared identity verification on Securitize's own platform. CEO Carlos Domingo described the intent plainly, the goal was to show what real shares onchain, not fake shares actually looks like.

It worked, at least as a headline. It is also one of the more interesting natural experiments this industry has run in a while, two very different blockchains carrying the exact same regulated asset, on the same day, under the exact same legal constraints. Whatever weaknesses exist in how each chain handles compliance-heavy tokens are now sitting under a real ticker, not a testnet demo.

This piece sets the stock price aside and goes straight at those weaknesses, the specific attack vectors Solana and Avalanche each introduce for tokenized equity, and what a team should actually be asking before choosing either one.

Solana's Compliance Layer Cuts Both Ways

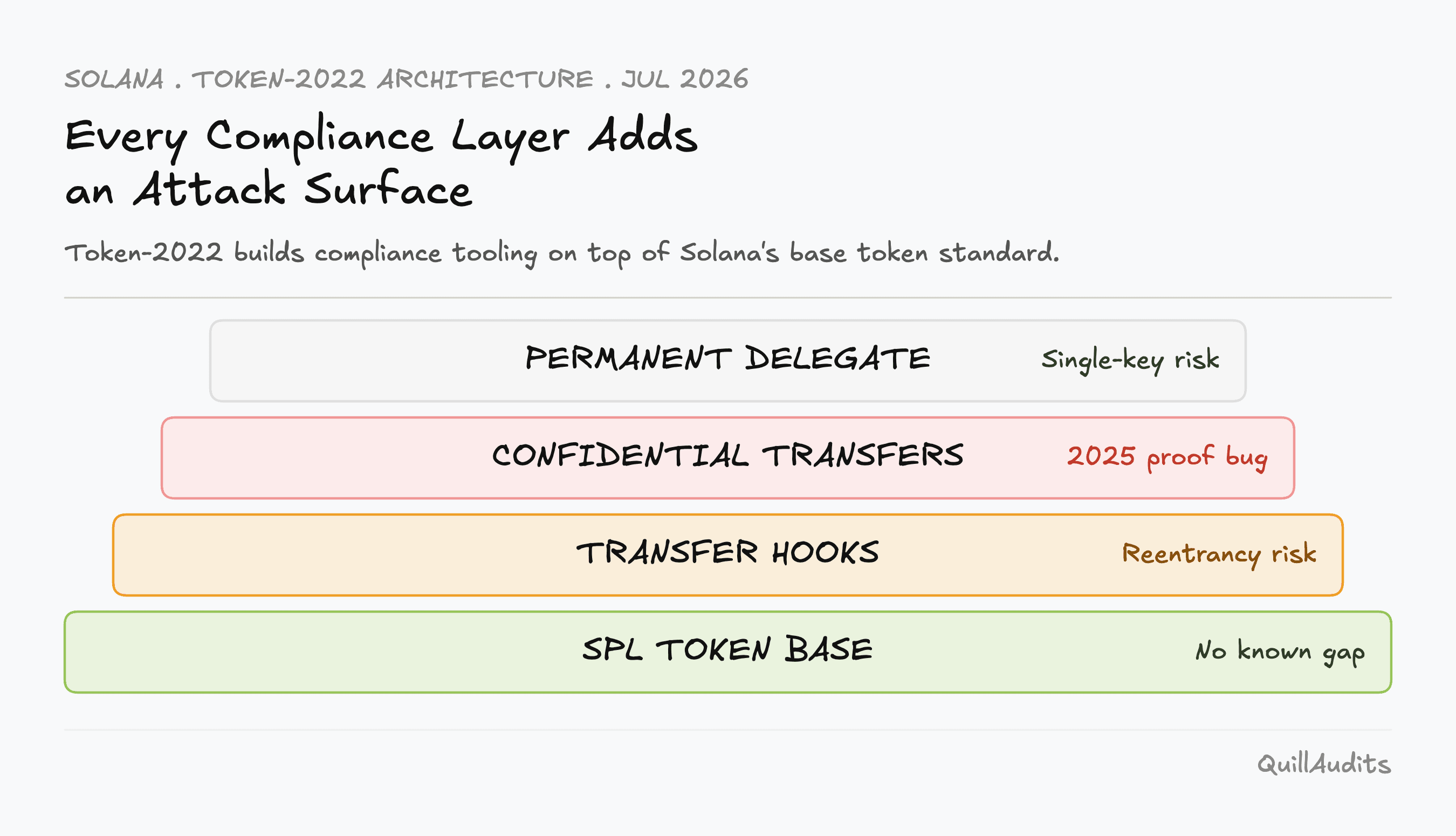

Most tokenized equity and real-world-asset issuers building on Solana do it through Token-2022, the chain's extended token standard. Token-2022 exists because the original SPL token standard had no native way to enforce the kind of restrictions a regulated security requires, who can hold it, who can be forced out of it, who can freeze it. Token-2022 solves that by shipping transfer hooks, a permanent delegate role, and default-frozen accounts as built-in extensions. An issuer gets real compliance tooling without writing a custom proxy contract from scratch.

The same extensions are also where the story gets more complicated.

Transfer Hook Reentrancy

Solana's account model was originally built in a way that made classic reentrancy attacks close to impossible. Programs could not casually trigger callbacks into arbitrary other code mid-transaction, the exact mechanism that has drained hundreds of millions of dollars out of Ethereum contracts over the years. Transfer hooks quietly reopened that door. A hook lets an issuer inject custom logic into every transfer of a token, handing execution to code the issuer does not fully control, unless that hook is written with the same checks-effects-interactions discipline Ethereum developers have needed for years. A team that treats Token-2022 as just SPL tokens with extra flags is exactly the team likely to ship a hook without that discipline, and reentrancy on a chain supposedly immune to it is not a theoretical risk anymore.

Confidential Transfer Proof Forgery

The clearest proof that this is not academic came in April 2025, when the Solana Foundation discovered a critical bug in the ZK ElGamal Proof program, the code that verifies confidential transfers under Token-2022. Confidential transfers let a holder move tokens without revealing the amount on a public ledger, exactly the kind of privacy feature an institutional issuer would want. The bug lived in the math. Some algebraic components had been omitted from the hash used in the proof's Fiat-Shamir transformation, and that omission meant a sophisticated attacker could forge a proof that looked completely valid, in theory minting tokens or moving funds out of accounts with no authorization at all. The Solana Foundation patched it within two days through a coordinated, private validator rollout, and no funds were ever lost. The confidential transfers feature itself was pulled from production afterward, pending further audit, worth confirming before assuming private settlement is actually available on any live issuance today.

Permanent Delegate and Freeze Authority Centralization

There is a third vector that gets less attention because it is not a bug at all. It is a design choice. Token-2022's permanent delegate can move any holder's tokens without that holder's signature, and the freeze authority can lock an account by default until it clears compliance checks. Both exist for good reason, a regulated security has to be recoverable from a sanctioned or compromised wallet. But both are also exactly the kind of centralized control point that security reviews exist to scrutinize, because a single compromised key holding either role does not cause a partial loss. It causes a total one, for every holder on that mint, at once.

Avalanche Trades Shared Security for Validator Control

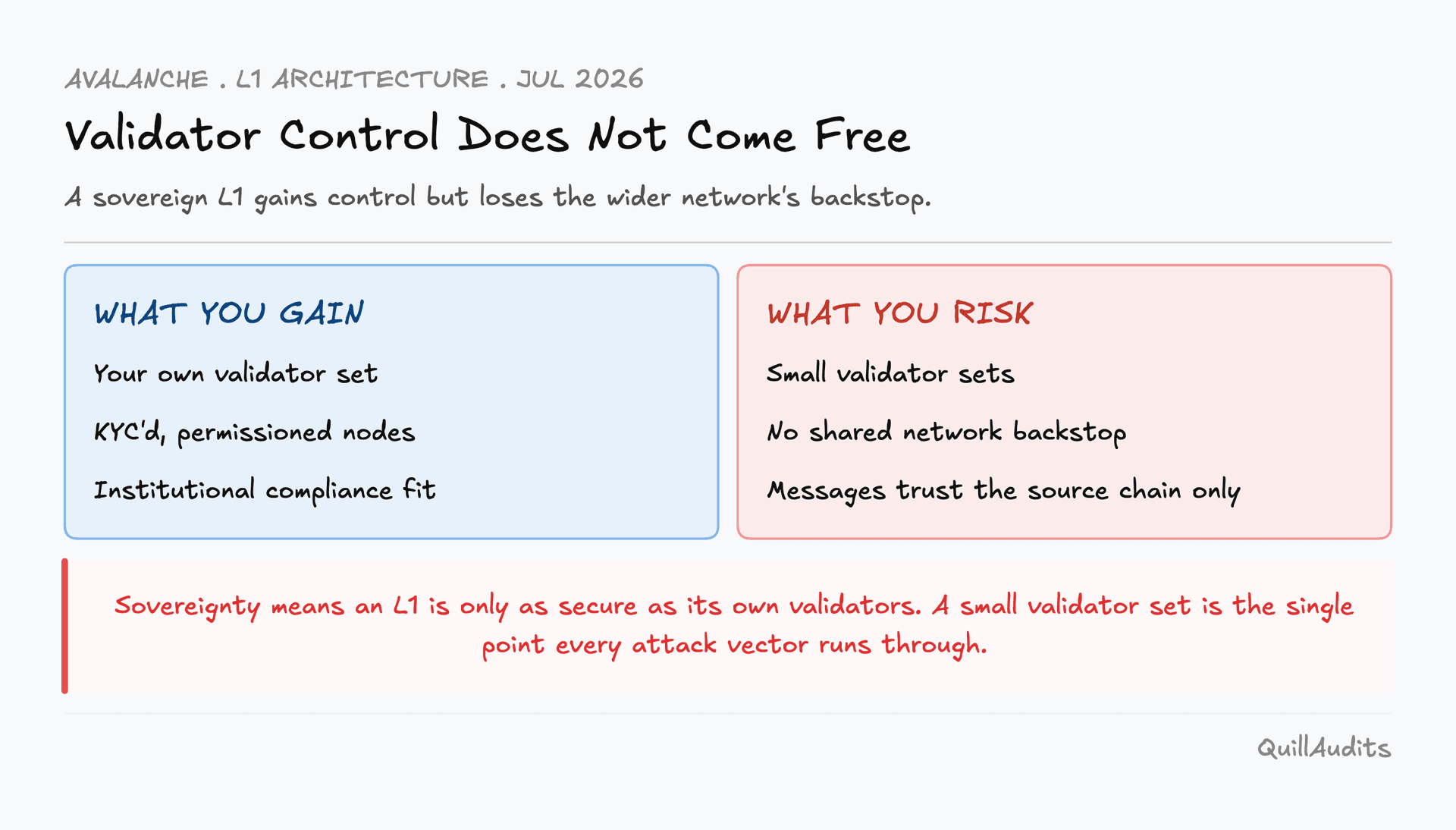

Avalanche's pitch to institutions starts from a completely different place. Instead of one shared chain that every issuer builds compliance logic on top of, Avalanche lets an issuer spin up its own sovereign L1, formerly called a subnet, with its own dedicated validator set. A bank that is legally barred from validating a fully public, permissionless chain can still participate in a chain where every single validator has been vetted, licensed, and KYC'd. That is a genuinely different value proposition than Solana's, and it is why permissioned Avalanche L1s have shown up in pilots involving major asset managers and banks running tokenized portfolio rebalancing and intraday settlement.

Sovereignty, though, is also where Avalanche's specific risks come from.

Validator Set Sovereignty

An Avalanche L1 does not inherit security from the wider network the way a rollup inherits security from its settlement layer. It is only as secure as its own validator set, full stop, and a brand-new L1 spun up for a single issuer's tokenization program can launch with a genuinely small number of validators. Avalanche's own governance discussions are candid about what that means in practice. If funds are bridged from the shared C-Chain into an L1 with only a handful of validators, and that validator set is compromised or colludes, the wider network is not going to fork itself just to protect a small chain's stolen funds. The security of anything that crosses between chains is capped by the weakest validator set anywhere along its path, never by the strongest one.

Warp Messaging Destination Validation Gap

The cross-chain messaging layer that makes this architecture work, called Avalanche Warp Messaging, has its own specific and documented gap. An independent security review found that Warp does not include a built-in check confirming which chain a message was actually meant for. A message built for delivery to Chain B could, in principle, be received and processed by Chain C, if the application on top of Warp does not implement that validation itself. That check is left entirely to whichever developer builds the messaging integration, which means the exact mistake that has caused cross-chain exploits elsewhere in the industry is fully possible here, the moment a team assumes the protocol is handling it for them.

Validator Removal and Asset Custody Risk

There is one more structural detail worth knowing. L1 staking tokens are not locked on the shared P-Chain, so a compromised or malicious L1 can remove its own validators at will, and any assets moved onto that L1 sit entirely under its own purview, with no backstop from the Primary Network. Avalanche's real-world-asset footprint, reported at roughly $370 million as of the first quarter of 2026, remains far smaller than Solana's, meaning fewer live deployments have actually stress-tested this custody model under real pressure.

What a Founder Should Actually Be Asking

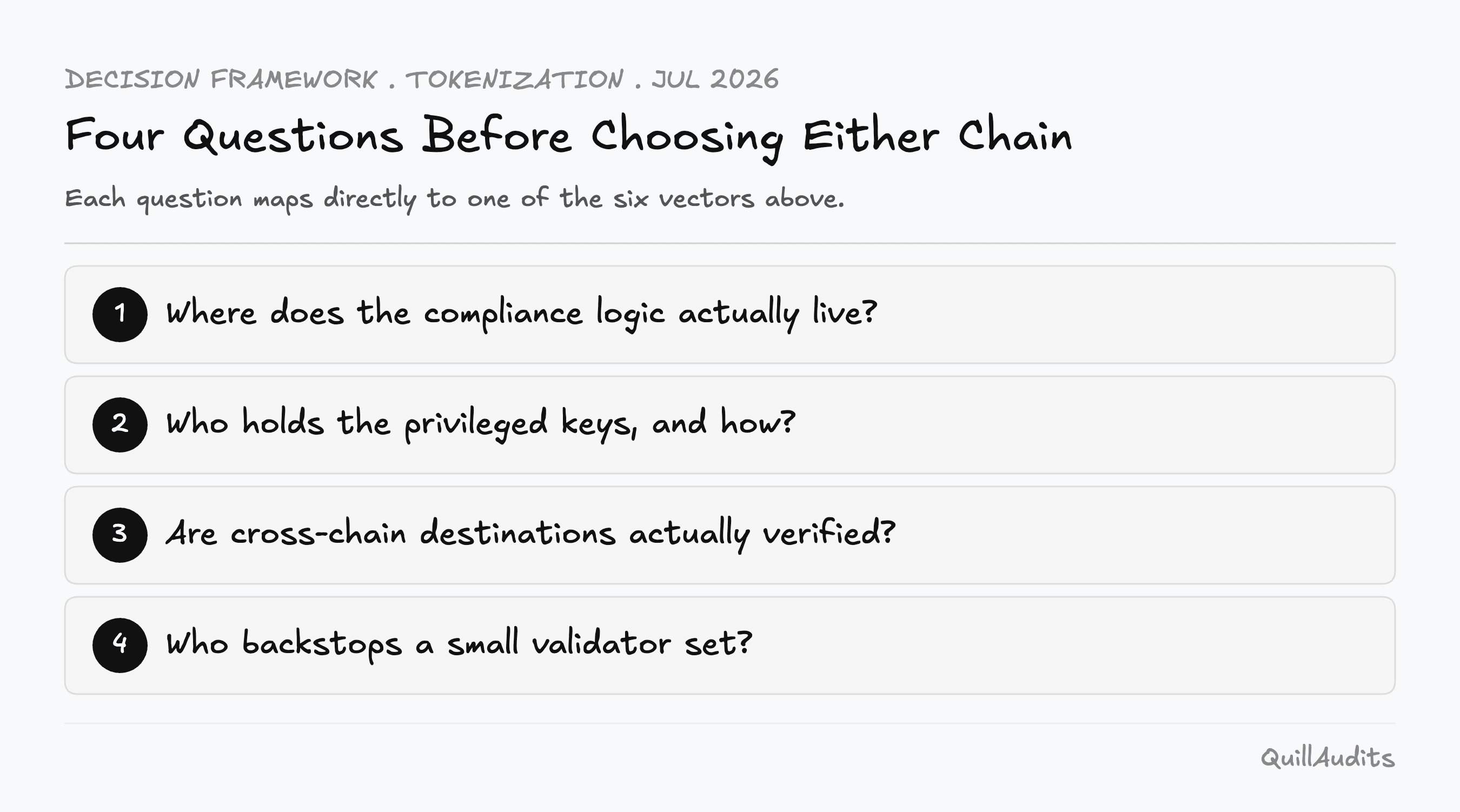

Neither of these chains is the wrong choice. Securitize just proved, in production, that both can carry a real, regulated, NYSE-listed security at once. But which chain is better is the wrong question for a team actually building this. The right questions are narrower, and map directly onto the vectors above.

Where the Compliance Logic Actually Lives

Ask whether the restrictions enforced on a token, who can hold it, who can be forced out of it, live inside a token standard extension that has already been through years of public scrutiny, or inside a custom contract your own team wrote in the last six months. Token-2022's transfer hooks and permanent delegate have had real adversarial attention. A bespoke compliance contract almost certainly has not, no matter how carefully it was written.

Who Holds the Privileged Keys

Every compliance model eventually comes down to a small number of keys, a permanent delegate, a freeze authority, or a validator set's aggregate signing key. Before choosing a chain, know exactly who holds each one, how it is stored, and what happens to every holder on that asset the day one of those keys is compromised.

Whether Cross-Chain Destinations Are Actually Verified

If the token moves across more than one chain, find out whether the messaging layer itself verifies which chain a message is meant for, or whether that verification is something your application has to build and maintain forever. Warp Messaging leaves this to the developer. Assuming otherwise is exactly how a misrouted message becomes a real loss.

Who Backstops a Small Validator Set

If the chain carrying the asset is a small, purpose-built L1 or subnet, ask directly who is backstopping it if its validators are compromised or collude. The honest answer, for most young chains, is usually nobody. That is not a reason to avoid the chain. It is a reason to size the validator set, and the security budget behind it, before real capital moves onto it.

Neither answer is universally correct. A team serving regulated institutions that cannot touch a permissionless validator set has real reason to accept Avalanche's sovereignty tradeoff. A team that wants native, battle-tested compliance primitives without maintaining its own validators has real reason to accept Solana's broader attack surface. The mistake is picking either one without asking these questions first, and learning the answers only after a compromised key or an unvalidated message has already moved real money.

Where This Is Actually Heading

The Market Size Debate

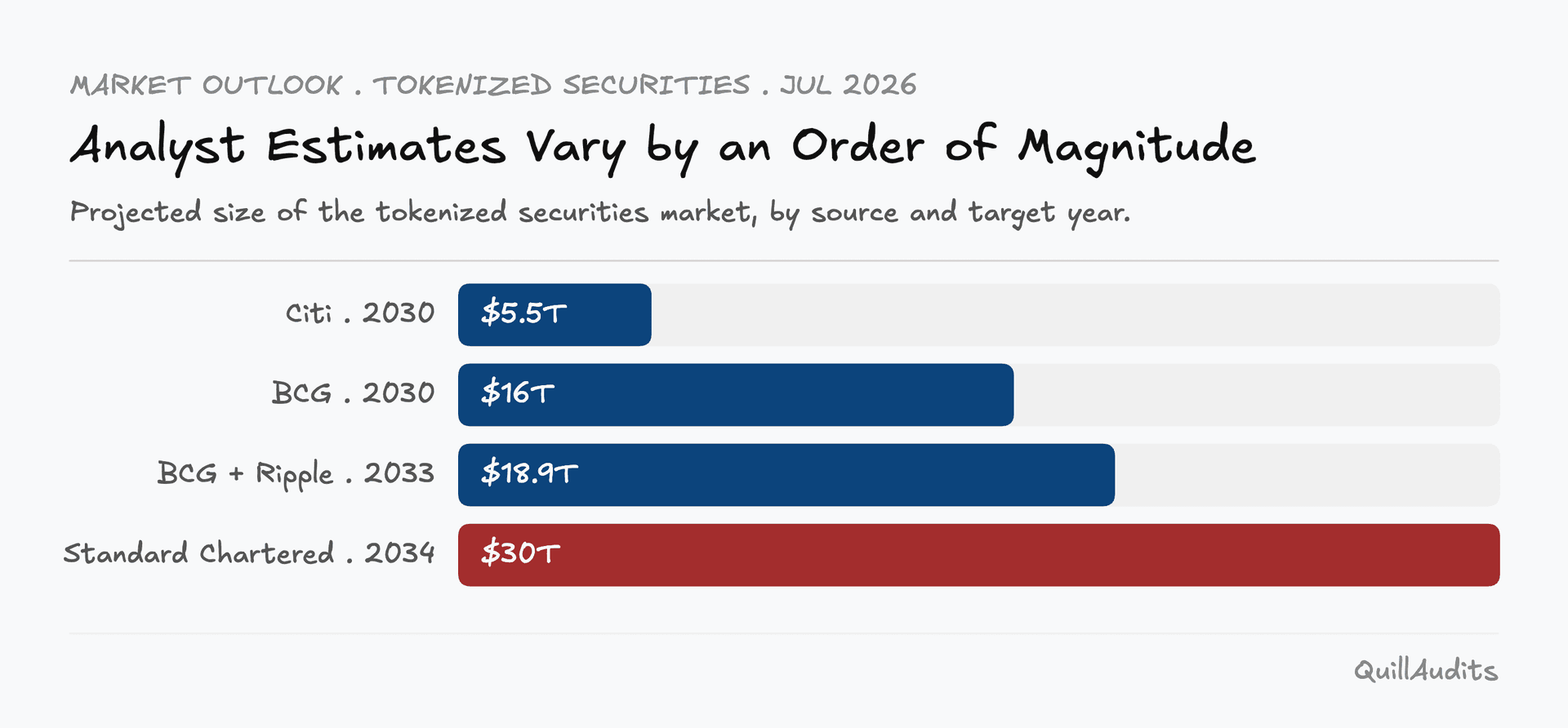

The market-size estimates for tokenized securities disagree with each other by an order of magnitude, depending on who is doing the estimating. Citi has projected the market could reach $5.5 trillion by 2030. Boston Consulting Group has put a broader tokenization figure at $16 trillion over the same horizon, and a joint BCG and Ripple estimate runs to $18.9 trillion by 2033. Standard Chartered's number is higher still, at $30 trillion by 2034.

What Actually Changes Structurally

Multi-chain issuance from day one, the way Securitize just did it, becomes standard practice rather than a headline-grabbing exception, shifting the hardest engineering problem from picking a chain to keeping compliance logic and privileged roles consistent across chains that do not share an execution model. Privileged roles like minting, freezing, and delegate authorities start getting the same scrutiny admin keys and upgrade authorities already get in DeFi, because the dollar value behind a single compromised key keeps climbing every quarter. Cross-chain messaging trust assumptions stop being an implementation detail and become a primary audit target, since both Token-2022's hooks and Avalanche's Warp Messaging show the interesting vulnerabilities increasingly live at the seams between systems, not inside any single contract. And privacy features like confidential transfers come back once they survive further scrutiny, because institutions will keep demanding private settlement without giving up composability.

Conclusion

Securitize's launch is a genuine achievement, real capital moving onto public chains under full regulatory compliance, not a hypothetical anymore. The six vectors above are not reasons to avoid either chain. They are the checklist. Anyone tokenizing real equity on Solana or Avalanche should have answers to every one of them before mainnet, not after.

Contents