A Founder's Guide to Tokenizing Money Market Funds and Private Credit

Tokenized money market funds and private credit are growing fast. Here is the custody, compliance, and security architecture founders need to get right.

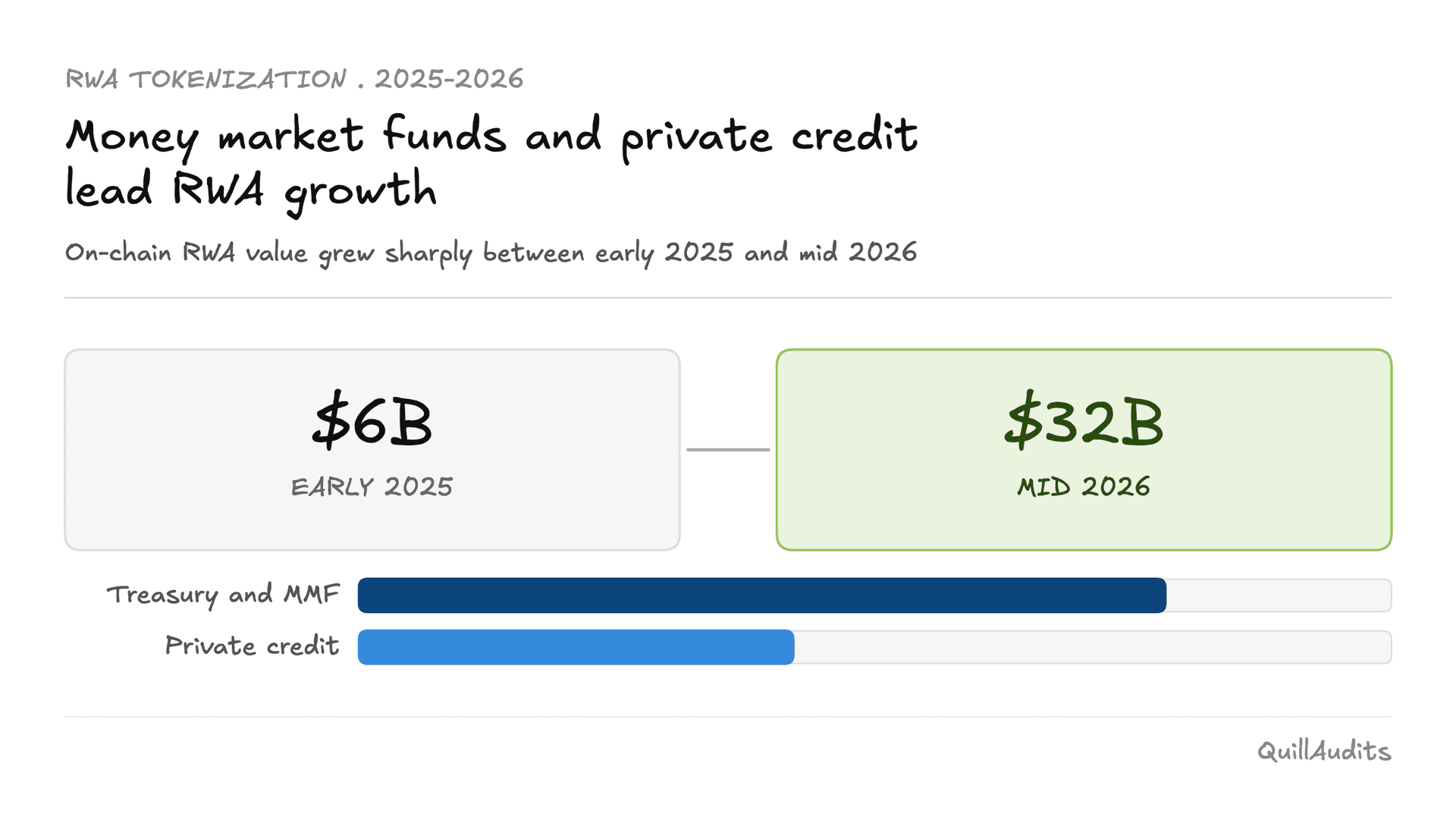

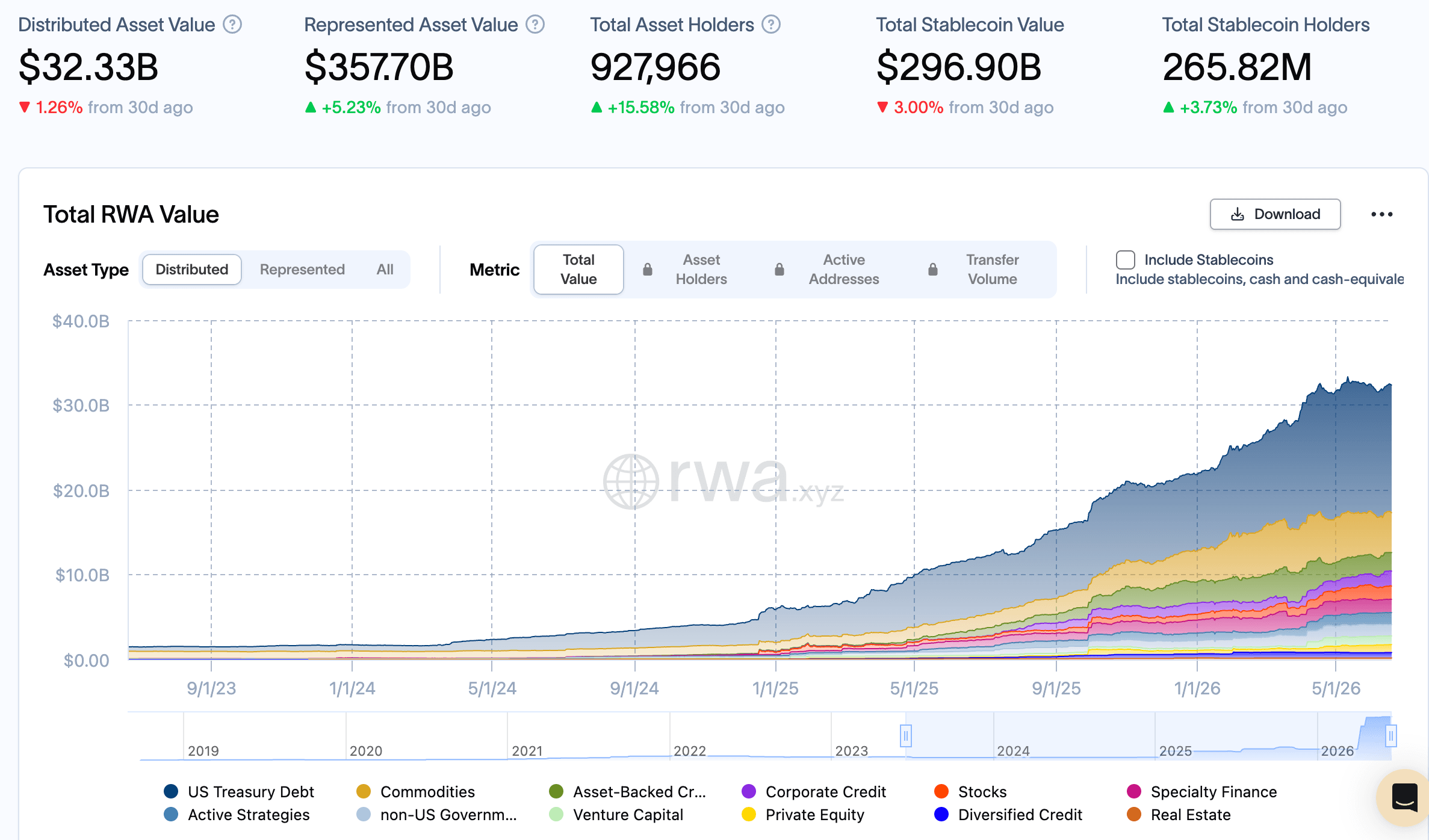

Tokenized real world assets grew from roughly $6 billion to more than $32 billion between early 2025 and mid 2026. Most of that growth sits in two categories that sound almost boring on paper, money market funds and private credit. The instruments are not new. What is new is the technical stack underneath them, the token standards, custody arrangements, oracle systems, and cross-chain infrastructure that now sit between an investor and the asset they think they own. This piece walks through how these instruments are actually built, what regulators now expect, and the security architecture that separates a fund that survives a stress event from one that does not.

How A Fund Or A Loan Actually Becomes A Token

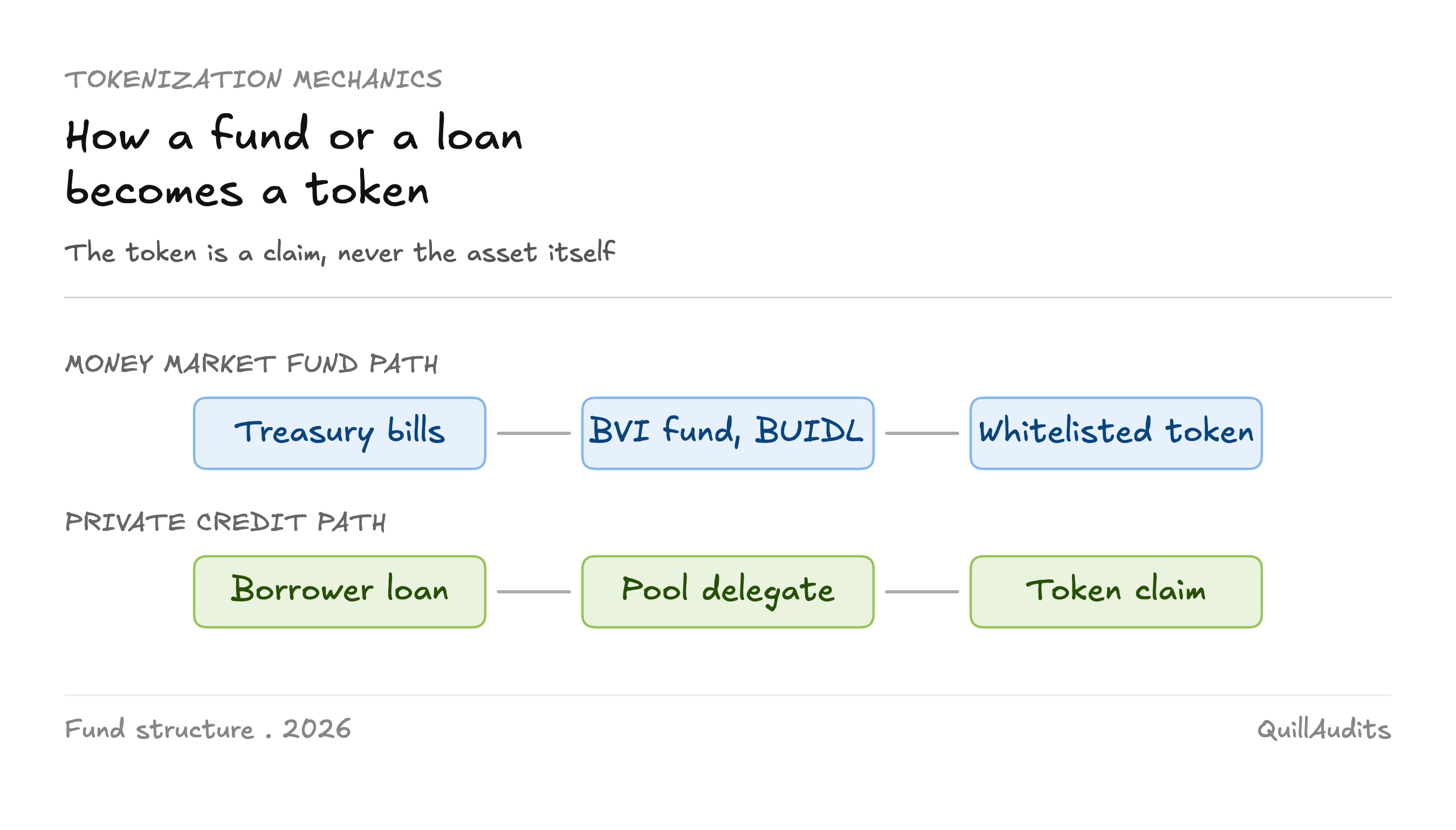

A tokenized money market fund still holds the same assets it always did, short term Treasury bills, notes, and repo agreements, inside a regulated legal structure. BlackRock's BUIDL fund, for instance, is structured as a British Virgin Islands limited company managed by BlackRock Financial Management, with Securitize acting as the technology and transfer agent layer. What changes with tokenization is the share class. Ownership moves from a row in a transfer agent's database to a token, and BUIDL's shares settle through a customized ERC-20 contract with a built in whitelist transfer control mechanism rather than an open, permissionless design. Franklin Templeton took a different legal path with its BENJI token, which represents shares in a US registered fund under the Investment Company Act of 1940, carrying the full protections that come with that regulatory status.

Private credit follows a similar pattern with more moving parts. A protocol structures a loan pool, underwrites a borrower off chain, originates the loan, and issues tokens to depositors who earn interest as the borrower repays. Maple Finance runs this through pool delegates, while Figure Technology Solutions tokenizes existing consumer debt such as home equity lines of credit directly, so the loan itself moves on chain rather than a fund share that merely represents it. In every case, the token is a claim on a legal structure, an SPV, a trust, or a regulated fund, that in turn holds the actual asset. The token is never the asset itself, and every layer between the claim and the asset is a place where something can go wrong independently of how the underlying asset performs.

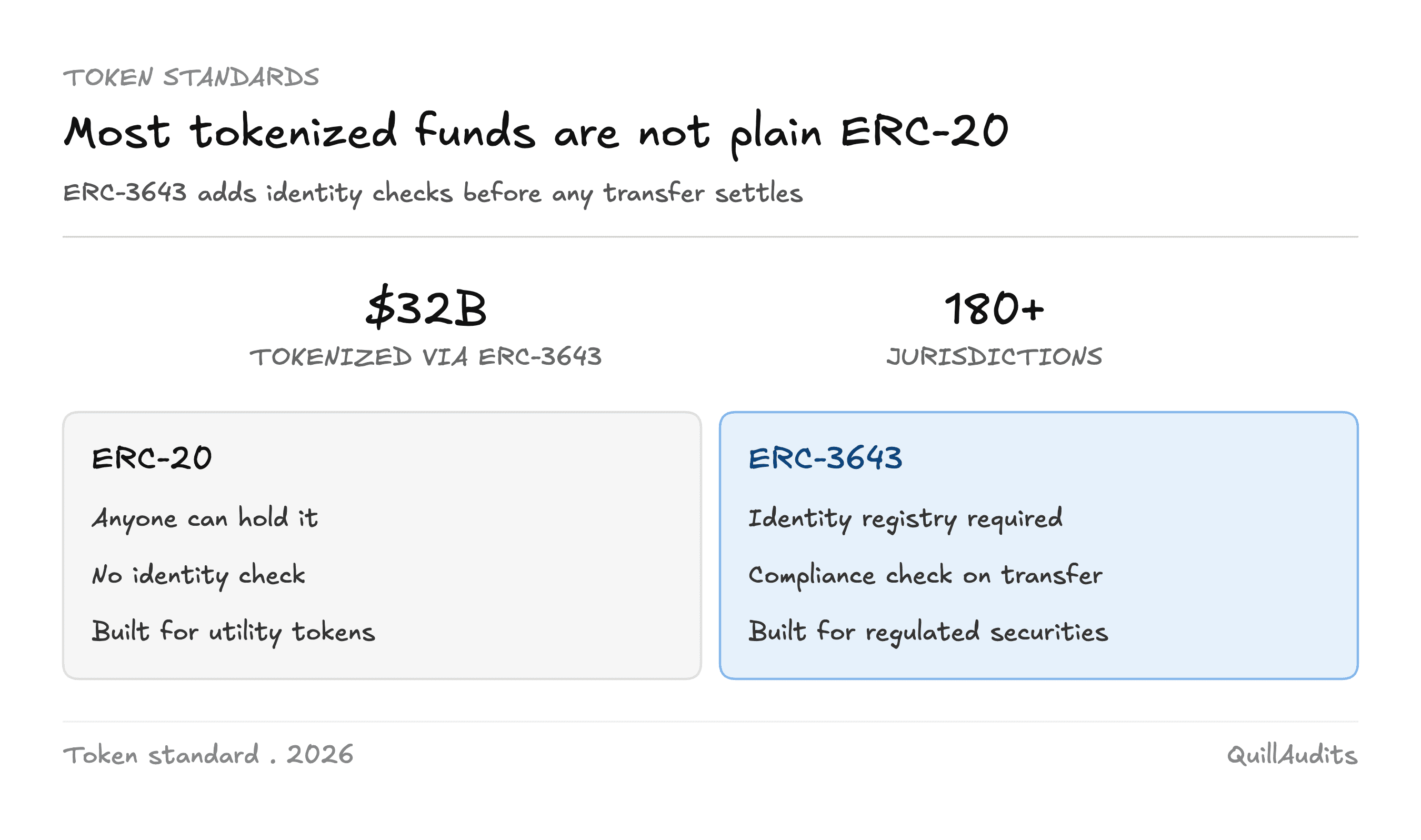

The Compliance Layer and Why Most Tokens Are Not Plain ERC20

A detail that gets skipped in most coverage of this space is that very few serious tokenized funds use a plain ERC-20 contract. ERC-20 is permissionless by design, anyone can hold or transfer the token, which is fine for a utility token and disqualifying for a regulated security. The standard that has emerged to fill that gap is ERC-3643, originally developed by the Luxembourg firm Tokeny under the name T-REX, and now governed by an independent association. ERC-3643 extends ERC-20 with mandatory identity verification through a linked identity registry, often built on the ONCHAINID framework, so that only wallets that have passed eligibility checks can hold or receive tokens, and every transfer is checked against the issuer's compliance rules before it settles on chain.

The adoption numbers explain why this matters. $32 billion in real world assets have been tokenized using ERC-3643 across over 180 jurisdictions, with institutional users including Franklin Templeton, Invesco, Apex Group, and Fasanara Capital, and infrastructure integrations from DTCC's ComposerX platform and the Monetary Authority of Singapore's Project Guardian. The US SEC chairman cited the standard by name in a 2025 speech on tokenization policy. The practical takeaway is that compliance is not a feature you bolt onto a token after launch. If a tokenized security moves to an ineligible wallet, that is a potential unregistered securities distribution regardless of intent, and no amount of off-chain paperwork undoes a transfer that has already settled on chain. The identity and eligibility logic needs to live inside the smart contract from the first line of code.

How Fast The Market Is Actually Moving

The growth curve in this category is unusual even by crypto standards. Tokenized real world assets climbed from about $6 billion to more than $32 billion in roughly sixteen months. Treasury backed products and money market funds still account for the largest share of that total, while active on chain private credit reached close to $19 billion by late 2025, with cumulative originations above $33 billion. What makes this growth different from earlier crypto cycles is who is funding it. JPMorgan now describes tokenized money market funds as the natural successor to stablecoins, built for institutions that want programmable cash rather than a static digital dollar, and the capital behind that view is sovereign wealth funds and large asset managers rather than retail speculation.

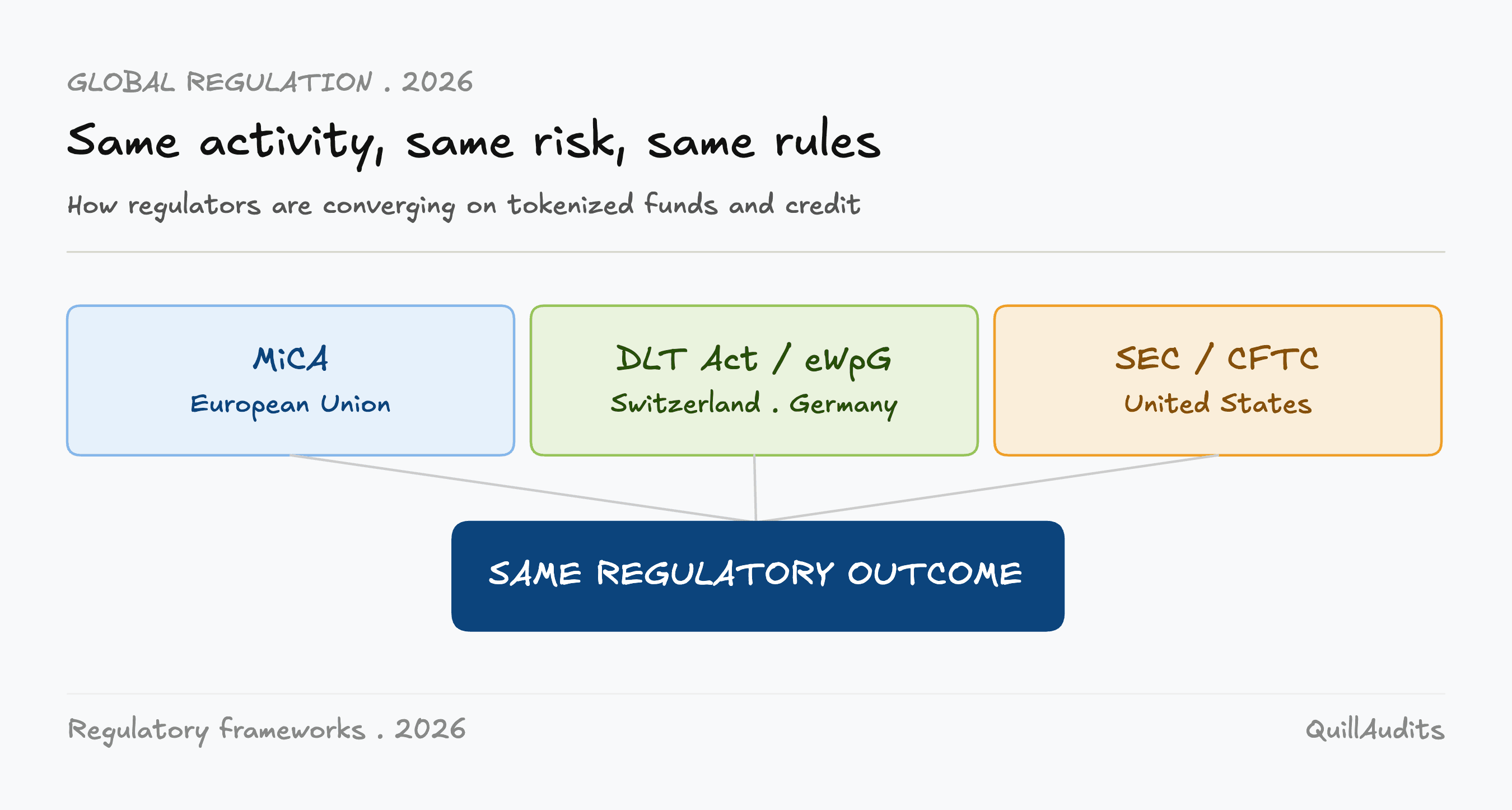

Regulation Has Moved From Grey Zone To Genuine Framework

Regulators have converged on a simple principle, same activity, same risk, same regulatory outcome, regardless of which rail the instrument settles on. In the European Union, MiCA now requires most tokenized money market and credit products to be classified clearly as securities or asset referenced tokens, with formal disclosure, reserve, and authorization requirements attached. Switzerland's DLT Act and Germany's eWpG have made it standard practice to structure these instruments as proper electronic securities on licensed infrastructure rather than informal tokens with vague economic rights. In the United States, the SEC and CFTC have both signaled that tokenized Treasuries and private credit will face the same custody, disclosure, and investor protection standards as their traditional counterparts. For a founder, the legal wrapper now matters at least as much as the smart contract sitting on top of it, and increasingly that contract needs to encode the legal logic directly through standards like ERC-3643.

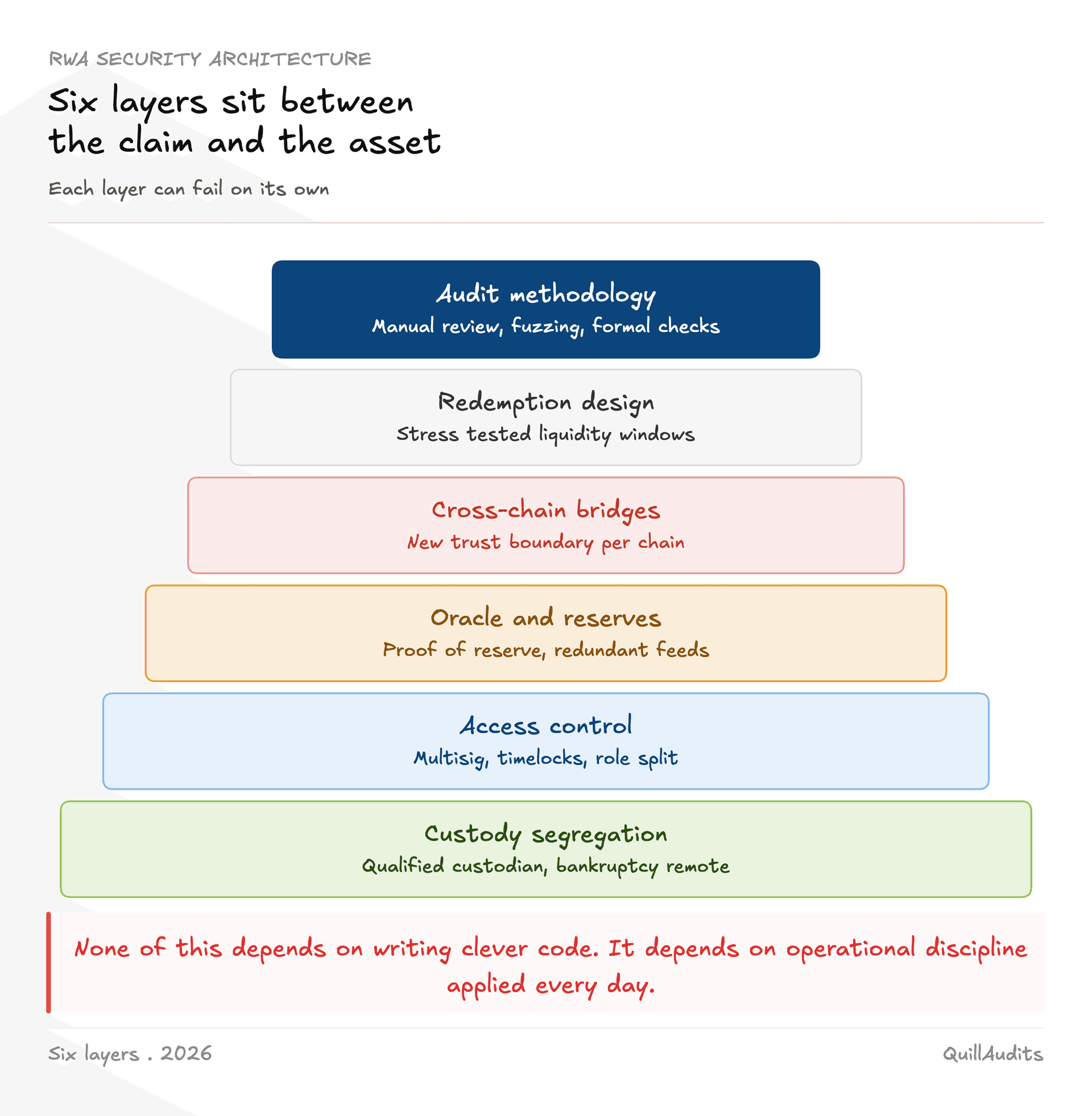

The Security Architecture, Where Tokenized Funds Actually Break

Once a token is understood as a claim rather than the asset, the security question becomes concrete. Every layer between the claim and the underlying asset is a place where something can go wrong, independently of whether the Treasury bill or loan is performing exactly as expected. None of the practices below depend on clever code. They depend on operational discipline applied consistently.

Custody is the foundation. Serious issuers use regulated qualified custodians rather than self-custody, and qualified-custodian status is a specific legal designation under rules such as SEC Rule 206(4)-2, not a marketing term. The institutional custody market for tokenized RWA in 2026 is dominated by a handful of regulated providers, including Anchorage Digital Bank, BitGo Trust, Fireblocks, Coinbase Custody, and Komainu, each carrying different insurance coverage. BitGo, for instance, carries a $250 million policy underwritten through Lloyd's of London. Assets need to sit segregated from the issuer's own balance sheet inside a bankruptcy remote structure, so an issuer's financial trouble cannot drag token holders into a creditor dispute over assets that were always supposed to be theirs.

Access control is the second layer. Anything capable of minting, freezing, pausing, or upgrading a contract should run through role based permissions, multisignature approval, and timelocks, so no single key and no single person can unilaterally change what a token represents. This matters more for permissioned tokens than ordinary DeFi contracts, because the compliance registry deciding who can hold a token is itself a privileged component. If that registry can be modified by a single key, the entire eligibility model collapses regardless of how well the transfer logic is written.

Oracles and reserve verification form the third layer. Static, one time attestations are no longer the standard institutions expect. Chainlink's Proof of Reserves system provides automated, periodic on chain attestations by querying custodian data through a decentralized oracle network, and in March 2026 BlackRock's BUIDL fund integrated Chronicle Protocol's Proof of Asset system for real time, independently verified attestations of holdings and custody data. Any price feed used for collateral valuation or redemption pricing needs redundancy and circuit breakers, because stale data can misstate a fund's value even when the underlying asset performs exactly as documented.

Cross-chain infrastructure is a newer fourth layer that most security checklists still underweight. BUIDL itself is no longer single-chain. It has expanded across nine networks including Ethereum, Solana, Arbitrum, Avalanche, Polygon, Optimism, Aptos, and BNB Chain, with Wormhole serving as the interoperability layer that has facilitated more than $70 billion in cross-chain transfers for tokenized funds from issuers including BlackRock, Apollo, and Hamilton Lane. Every bridge or messaging layer introduced to make a token portable across chains is also a new trust boundary, and a compromise there can affect holders on every connected chain at once, not just the chain where the flaw originated.

Redemption design is the fifth layer, where liquidity risk and contract risk intersect. BUIDL's redemption process requires requests to be received by the transfer agent within a defined daily window to achieve same day settlement, mirroring traditional fund operations but still needing to be tested for what happens if a chain experiences congestion exactly when a wave of redemption requests arrives. Redemption logic only tested under calm conditions is not tested.

Finally, audit methodology needs to go beyond a single manual review. A serious security process combines manual line by line review of the compliance and access control logic, automated fuzzing of transfer restrictions and redemption math, and increasingly formal verification of the invariants that matter most, such as the rule that total token supply must always equal the custodied reserve balance reported through the proof of reserve feed. An audit performed once before launch, with no ongoing monitoring of custody, oracle, and bridge dependencies, leaves exactly the layers most likely to fail unchecked.

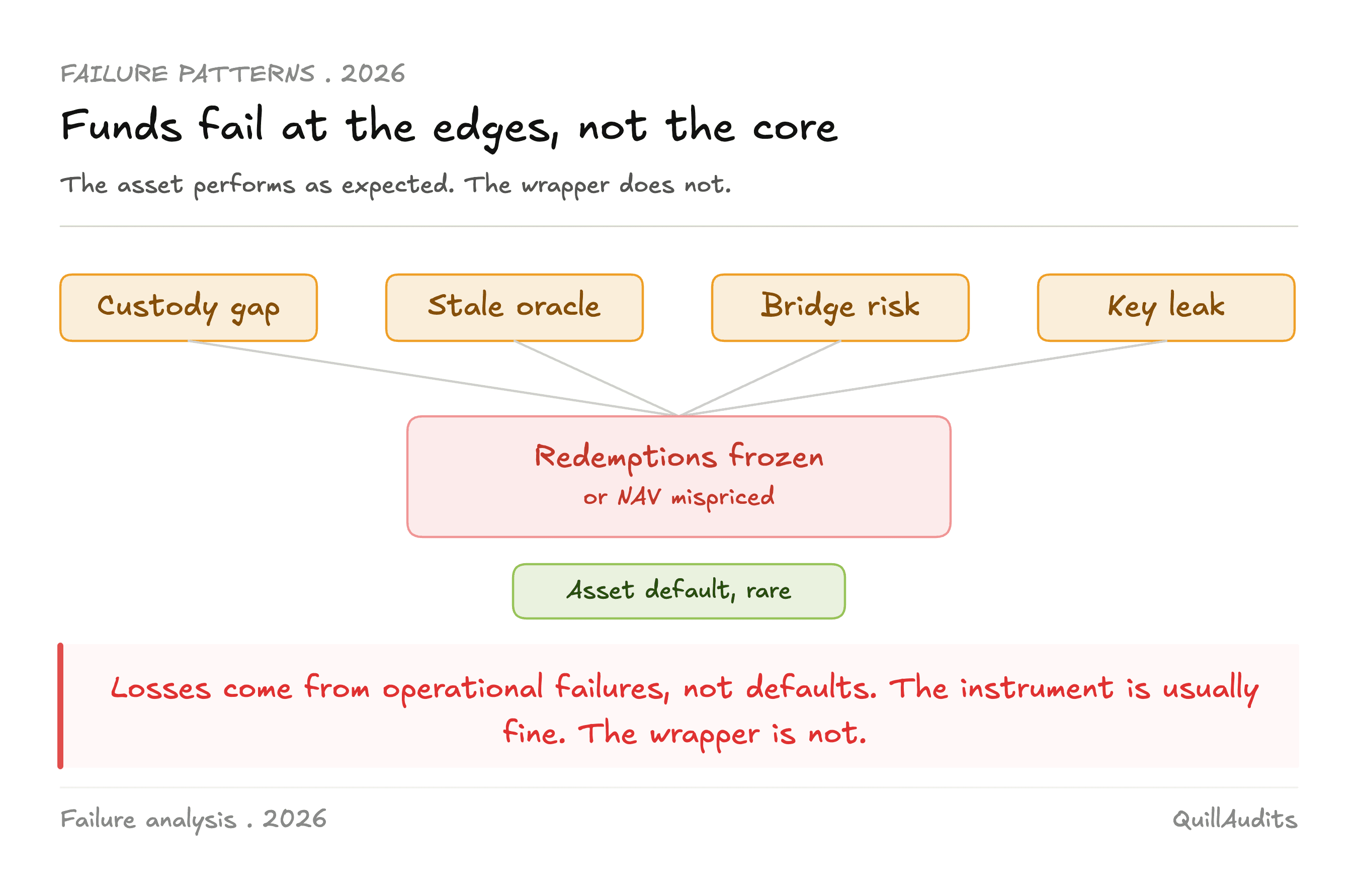

Where Tokenized Funds Actually Fail

The pattern across this category so far is consistent. Losses tied to real world asset tokenization have come overwhelmingly from operational failures, key management mistakes, oracle and data integrity issues, and bridge level compromises, not from the underlying Treasury bill or loan defaulting. A custody gap, a single admin key sitting in a hot wallet, a stale price feed, or a vulnerability in a cross-chain messaging contract can each independently freeze assets, mis-price a fund's net asset value, or block redemptions, even while the bond or loan behind the token performs exactly as expected. That asymmetry, where the financial instrument is conservative but the technical wrapper introduces new risk, is the central fact founders in this space need to internalize.

What This Means For Founders Building It

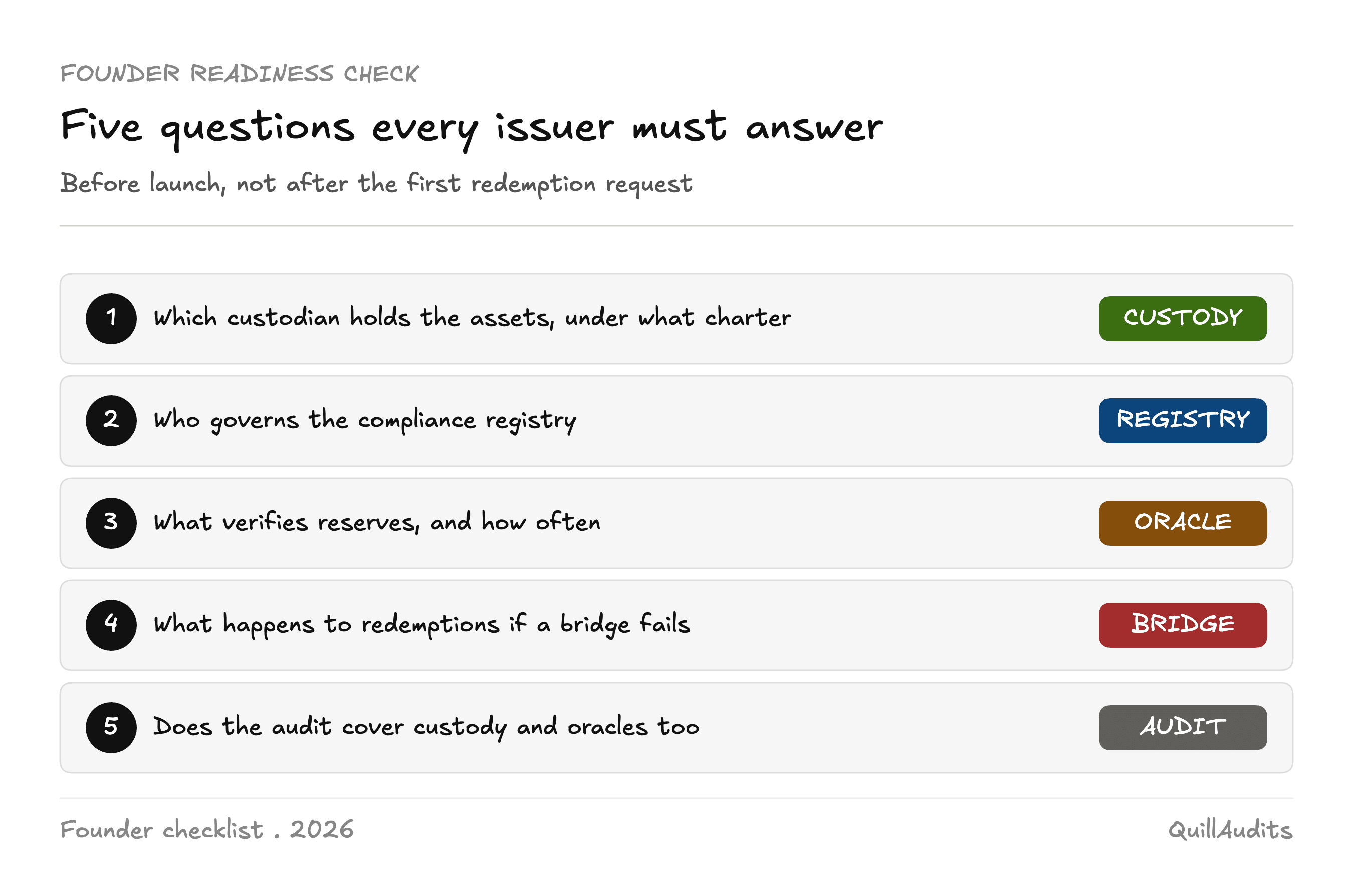

The founders who win the next phase of this market will not be the ones with the cleverest yield mechanism. They will be the ones who can answer, in detail, a specific set of questions, which qualified custodian actually holds the assets and under what charter, how the compliance registry is governed and who can modify it, what oracle and proof of reserve system verifies the fund's holdings and how often, what happens to redemptions if a chain or a bridge goes down during a liquidity event, and whether the audit process covers custody, oracle, and cross-chain dependencies or only the core transfer contract. Tokenizing money market funds and private credit is, underneath the on chain language, an old craft wearing a new front end. The instruments are not new. The compliance layer, the custody architecture, and the interoperability infrastructure are, and that is exactly where the engineering discipline now needs to live.

Conclusion

Tokenized money market funds and private credit are growing faster than almost any other category in on chain finance, and regulators have already converged on a clear standard, same risk, same rules. The instruments themselves are conservative. The risk sits in the custody, identity, oracle, and bridge layers built around them, and that is exactly where security work, not yield design, decides which issuers actually scale.

Contents