Six Crypto Neobanks Raised $200M in 90 Days. None Have a CISO.

Stablecoin banking is scaling fast, but security ownership is lagging. Explore why audits alone are not enough for long-term resilience.

Somewhere between a DeFi protocol and a traditional bank, a new category of financial product is quietly taking shape. Crypto neobanks. Stablecoin-native, mobile-first, borderless, and faster to spin up than anything the legacy banking system has ever produced.

They are also, in most cases, operating without the security infrastructure those ambitions demand.

This piece is about what the ideal version looks like, where the real ones fall short, and why the regulatory environment arriving in 2026 is going to force a reckoning that many of these platforms are not ready for.

What a Crypto Neobank Actually Is

The term gets used loosely, so it is worth being precise. A crypto neobank is a consumer-facing financial product that delivers banking-style services, current accounts, savings yield, debit card spending, cross-border transfers, and lending, through blockchain-native infrastructure rather than traditional banking rails.

The stablecoin is the foundation. Instead of a fiat deposit sitting in a fractional reserve system, user funds are held as USDC, USDT, or a similar asset, often earning yield through DeFi protocols under the hood. The card product connects that on-chain balance to Visa or Mastercard rails. The mobile app makes it look and feel like Revolut or Monzo.

Under the surface, it is a completely different machine. And it introduces a completely different threat model.

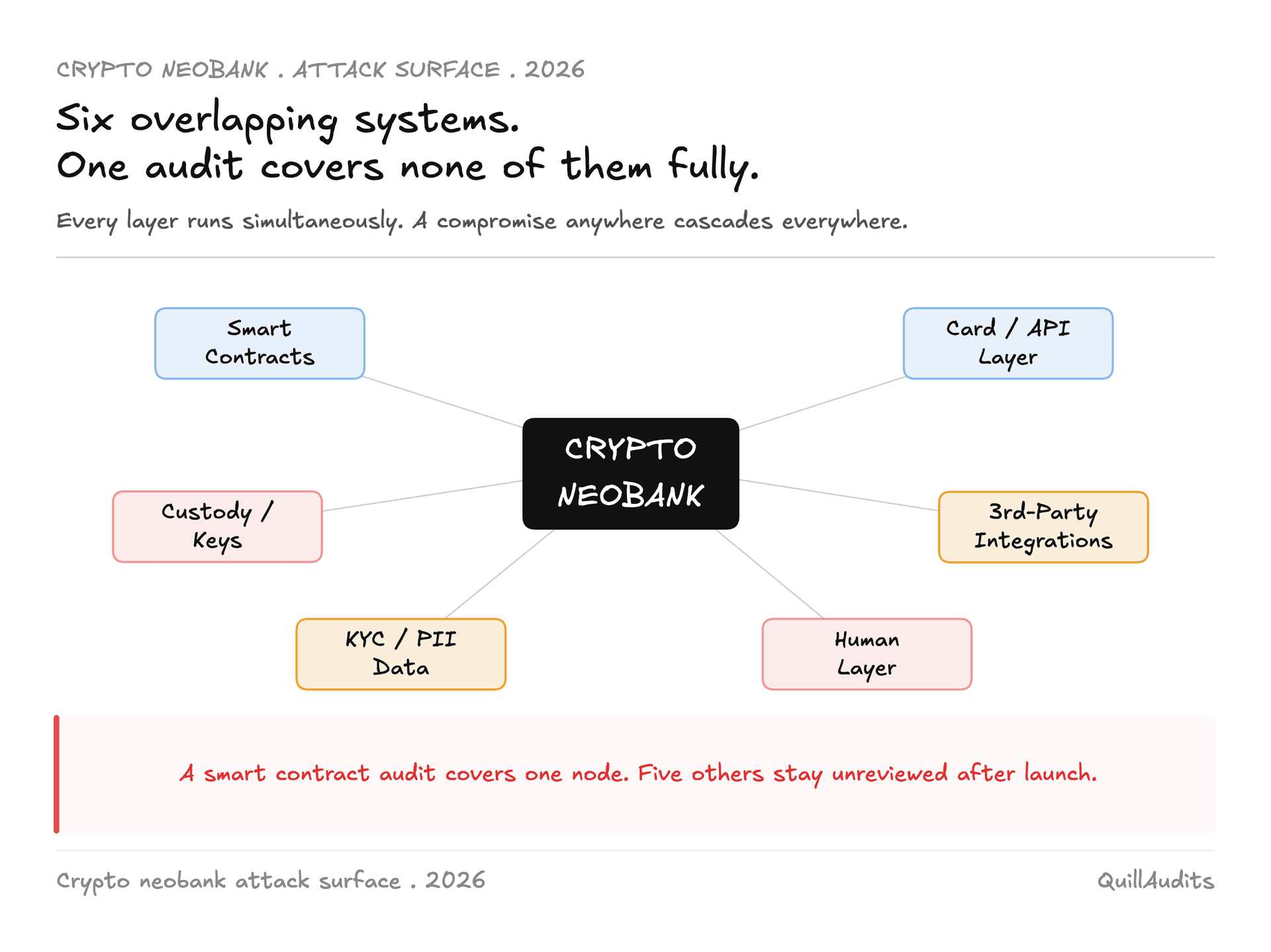

The attack surface of a crypto neobank is not one thing. It is several overlapping systems running simultaneously: smart contracts managing stablecoin vaults, API layers connecting to card issuers, custody infrastructure holding private keys, KYC databases, third-party yield integrations with their own risk profiles, and human teams managing all of it, often without formal security training.

A traditional bank has decades of regulatory pressure and internal audit culture, forcing it to manage each of these layers. A crypto neobank, in most cases, has a pre-launch smart contract audit and good intentions.

The CISO Gap Nobody Is Talking About

Six blockchain-native neobanks raised over $200 million in the last 90 days. Collectively, they are processing billions in annualized transaction volume. They hold real user deposits. They issue real cards. They operate across multiple jurisdictions with real regulatory exposure.

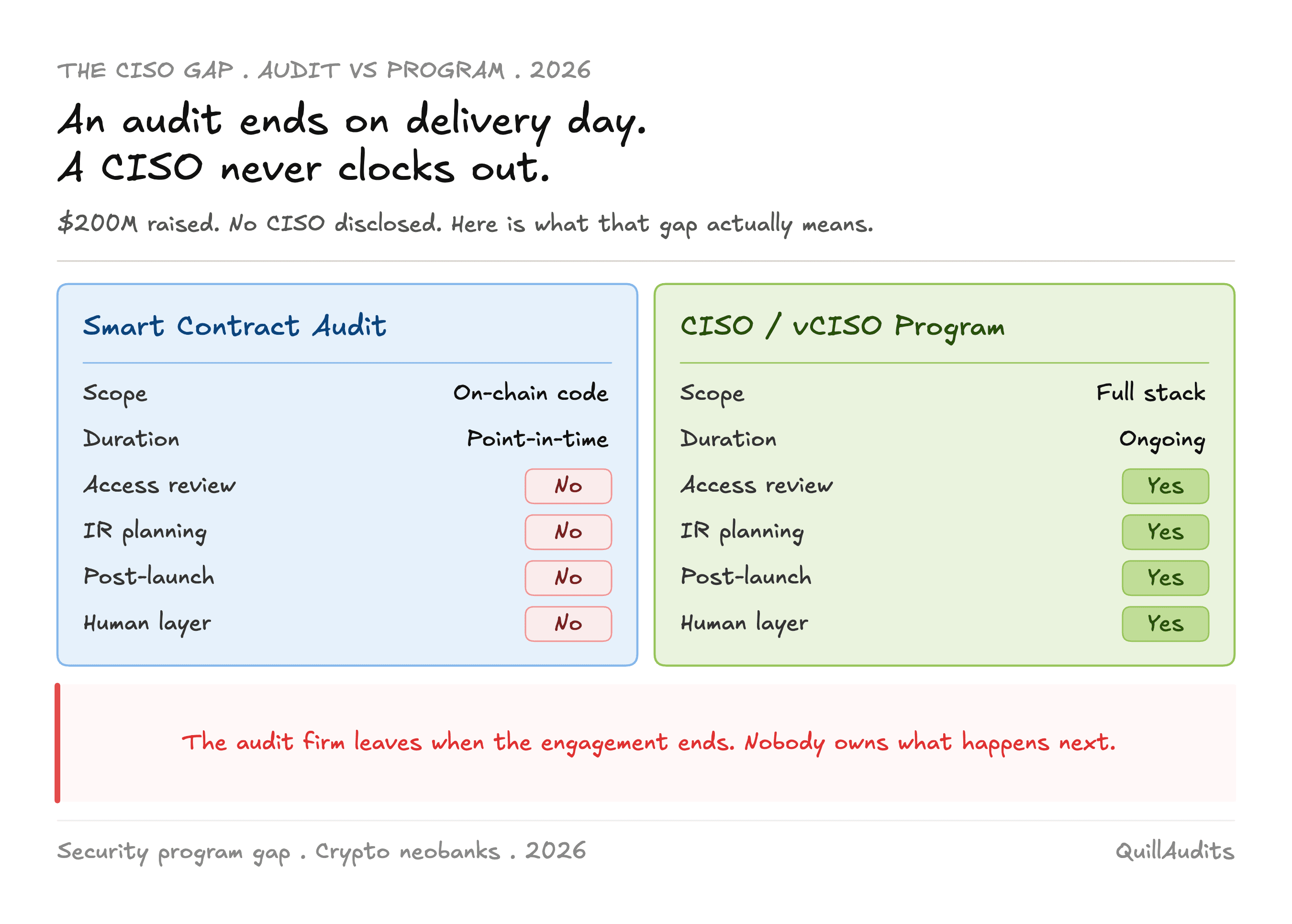

None of them have publicly disclosed a Chief Information Security Officer.

That is not an accident or an oversight in a job posting. It reflects something structural about how this category of company thinks about security. The assumption, often unstated, is that a smart contract audit before launch covers the security function. It does not. An audit is a point-in-time review of on-chain code by an external firm. It does not create a security program. It does not assign ownership to the functions that keep a live financial product safe after launch. It does not follow up.

What a CISO provides is continuity. The audit firm leaves when the engagement ends. The CISO stays. They own the access governance process that ensures no former developer is holding live admin keys six months after they stopped working on the project. They own the incident response plan that defines what happens in the first 30 minutes when anomalous on-chain activity appears at 3AM. They own the security review that happens before a new yield integration goes live, before a new chain is added, before a new card program manager is onboarded.

In traditional finance, the absence of a CISO at a company operating at this scale would be a regulatory red flag. In crypto, it is still treated as normal. That is the gap.

The cost argument gets raised often. A senior security executive with blockchain-native experience is a $400,000 annual hire before team or tooling costs. For a neobank at the $20M or $50M funding stage, that feels like a Series B problem. But the Infini exploit happened at $50M in TVL. The developer had been gone for over 100 days. The key was still live. Nobody had been assigned to check.

Waiting for scale to hire a CISO is the same logic as waiting for a fire to buy an extinguisher. By the time the problem is visible, the window to prevent it has already closed.

What the Ideal Security Stack Looks Like

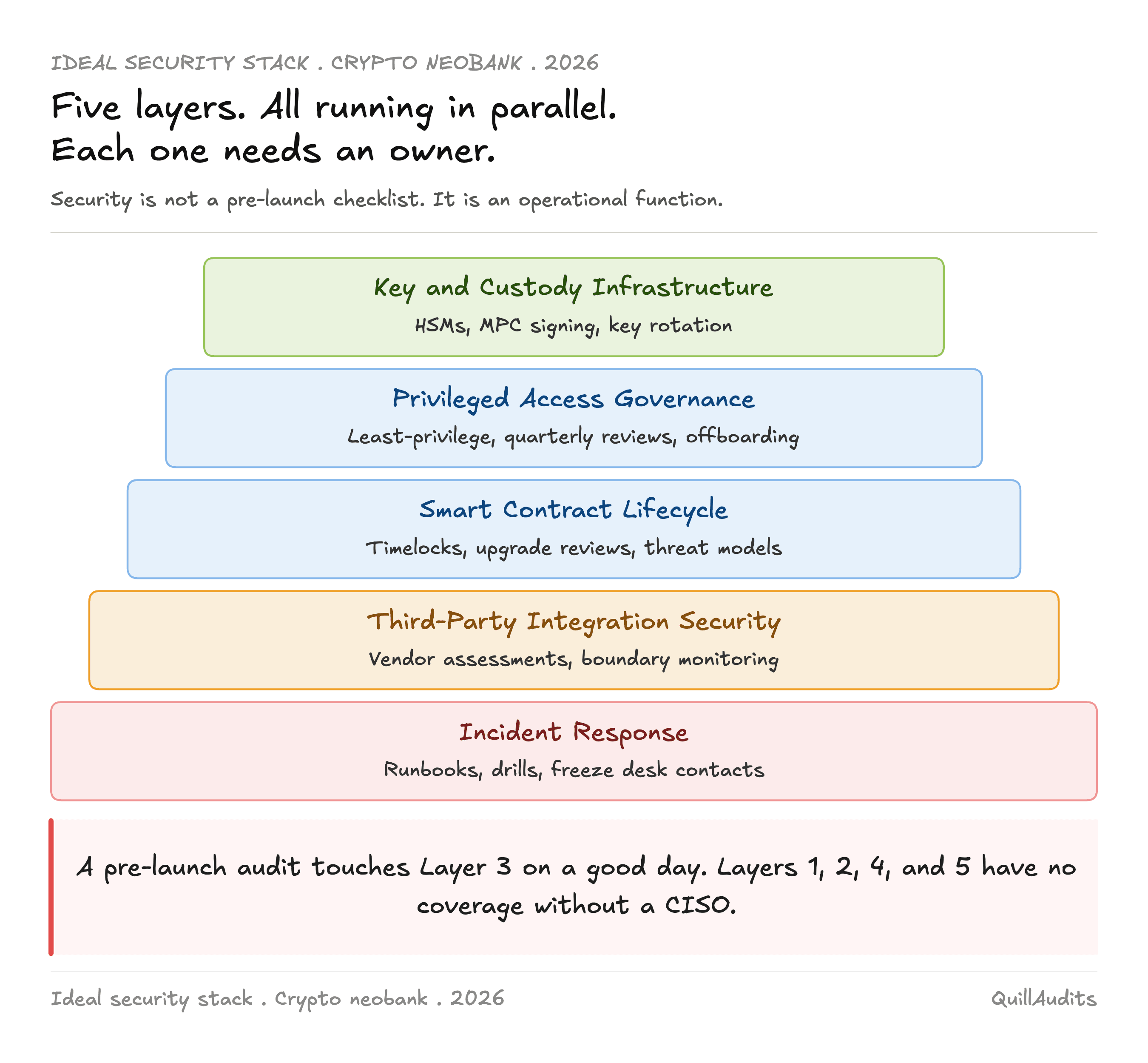

Before getting to what is broken, it helps to describe what good looks like. The ideal crypto neobank runs security as an operational function, not a pre-launch checklist. That means five layers working in parallel, not in sequence.

Key and custody infrastructure. Private keys that control user funds are never stored on a single server. Hardware Security Modules handle key generation. Signing requires multi-party computation or threshold signatures across geographically distributed nodes. Key rotation happens on a defined schedule. Recovery procedures are documented, tested, and controlled by named individuals with formal access approvals.

Privileged access governance. Every admin role, every operator key, every contract deployment wallet is documented. Access is granted on a least-privilege basis, reviewed quarterly, and revoked automatically when an engagement ends. Offboarding triggers a security checklist that cannot be closed without confirming access revocation. There is a single owner for this process.

Smart contract lifecycle management. The audit happens before deployment, but the security function does not end there. Upgrade paths are governed by timelocked multisig with a defined quorum. Every upgrade goes through an internal security review before it reaches governance. New integrations, new chains, new yield strategies each get a threat model before they go live.

Third-party integration security. The neobank does not build everything. Card issuers, on-ramps, off-ramps, yield protocols, KYC vendors: each one is a trust boundary. The ideal platform has a formal security assessment requirement for every integration partner, contractual security obligations baked into vendor agreements, and monitoring that covers integration boundaries, not just native contracts.

Incident response. Not a plan that lives in a Google Doc. An operational runbook with named contacts, defined escalation paths, tested communication protocols, and a relationship with the stablecoin issuer's freeze desk built before it is ever needed. The first time the team runs through the plan should not be during the incident.

Every one of these layers requires a human owner. That is what a CISO is. Not a title, not a compliance line item. A function.

What Actually Goes Wrong

The gap between the ideal and the reality is where the money goes.

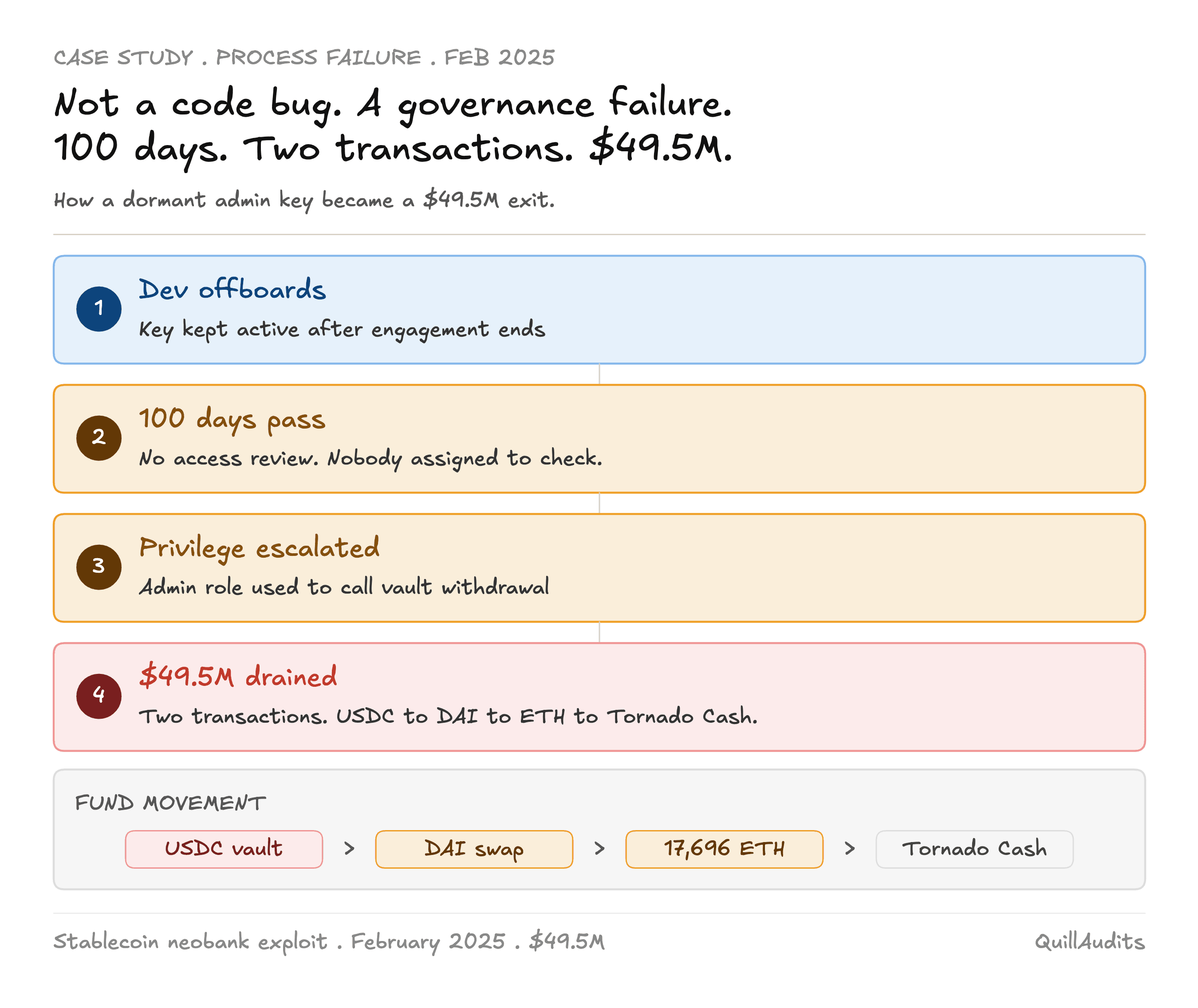

In February 2025, a stablecoin-focused neobank based in Hong Kong lost $49.5 million in a single exploit. The attack did not involve a novel vulnerability. It did not require sophisticated tooling. A developer who had built part of the platform's smart contract infrastructure retained administrative privileges after their engagement ended. Over 100 days passed. Then, in two transactions, the vault was drained. $11.45M, then $38.06M. USDC converted to DAI, swapped to ETH, routed through Tornado Cash.

The root cause was unambiguous: compromised access and privilege escalation. A contract role with vault withdrawal rights had never been revoked. Nobody had reviewed it. Nobody owned the process of reviewing it.

This is the pattern. Not exotic attacks. Process failures. The absence of ownership for security functions that are not covered by any audit scope. Privileged access that outlasts the engagement. Upgrade paths with no governance controls. Third-party integrations that nobody assessed before they went live. Social engineering campaigns targeting developers whose names and GitHub handles are publicly visible. These are the vectors that take platforms down, and they are invisible to any point-in-time code review.

The Regulatory Pressure Is Coming From Both Sides

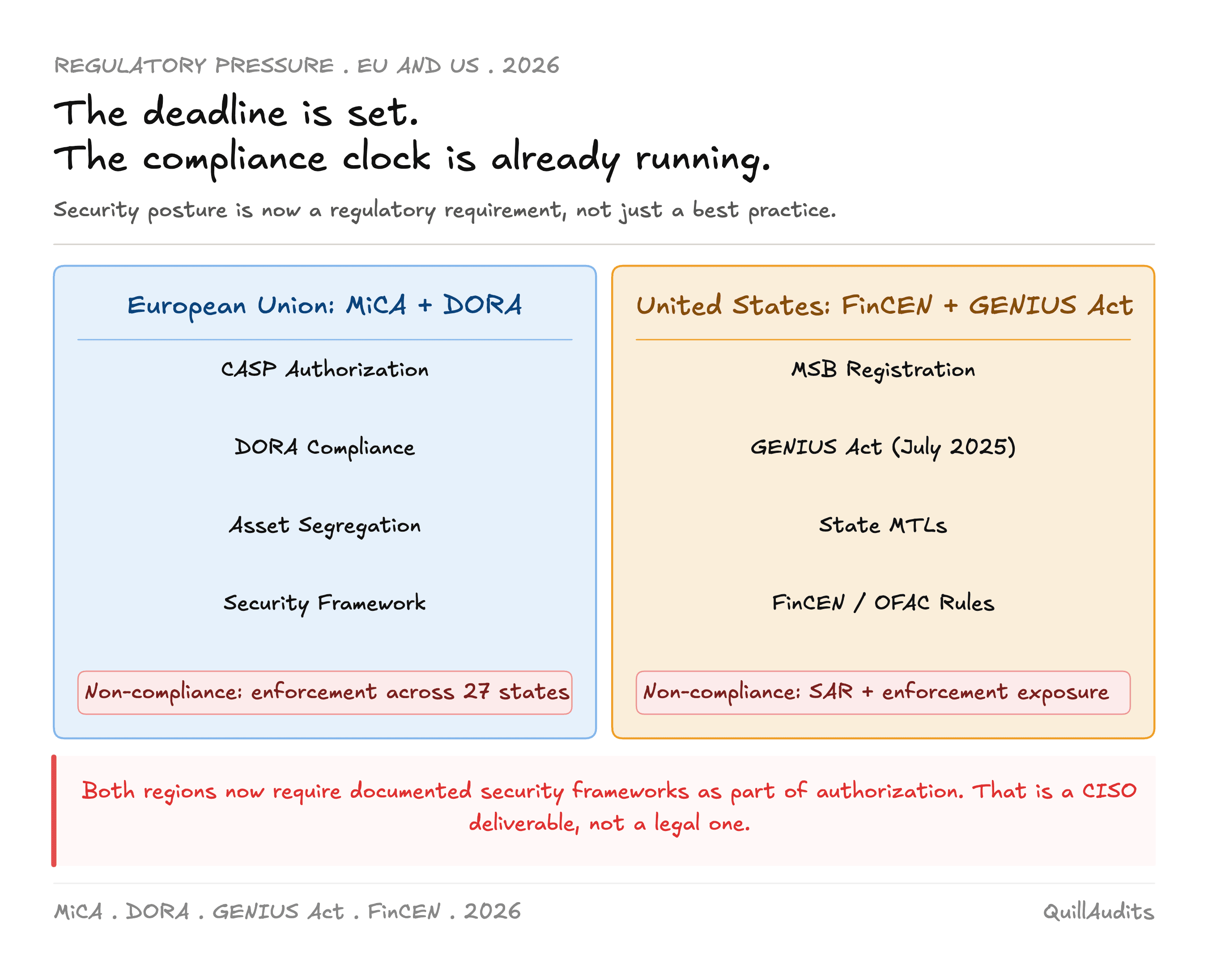

Here is the part most crypto neobank founders are not spending enough time on. The regulatory environment in 2026 does not give these platforms the luxury of treating security as a growth-stage problem to solve later.

In the European Union, MiCA is fully in force. The transitional period for existing crypto-asset service providers ends on July 1, 2026. After that date, any platform serving EU customers without a CASP authorization faces enforcement, shutdown orders, and blacklisting across all 27 member states. The authorization is not a rubber stamp. MiCA requires CASPs to demonstrate proper segregation of customer assets from company funds, stringent data protection measures, comprehensive AML and KYC procedures, and documented security frameworks across the full operation.

DORA, the Digital Operational Resilience Act, adds further requirements for all MiCA-licensed entities, covering ICT risk management, incident reporting obligations, operational resilience testing, and third-party technology risk. A crypto neobank operating in the EU without a formal security program and documented incident response capability is not just exposed to hackers. It is exposed to regulators.

In the United States, the picture is fragmented but moving fast. Any platform that exchanges, transfers, or custodies digital assets for US customers is classified as a Money Services Business under FinCEN, which triggers a written AML program, a designated Compliance Officer, Suspicious Activity Report obligations, and state-level Money Transmitter Licenses in 49 states. New York's BitLicense and California's DFAL are the most demanding of these regimes.

The GENIUS Act, signed into law in July 2025, created the first federal framework specifically for payment stablecoin issuers, requiring full reserve backing, monthly audits, and AML compliance supervised by the OCC. FinCEN and OFAC have since proposed additional rules implementing those obligations, with final implementing regulations expected before January 2027.

The convergence point is this: both the EU and the US are now building regulatory expectations around security posture, not just financial compliance. Documented security frameworks, incident reporting procedures, operational resilience testing. These are things a CISO builds. They are not things a founding team produces on their own in the weeks before a regulatory deadline.

The Threat Model in 2026

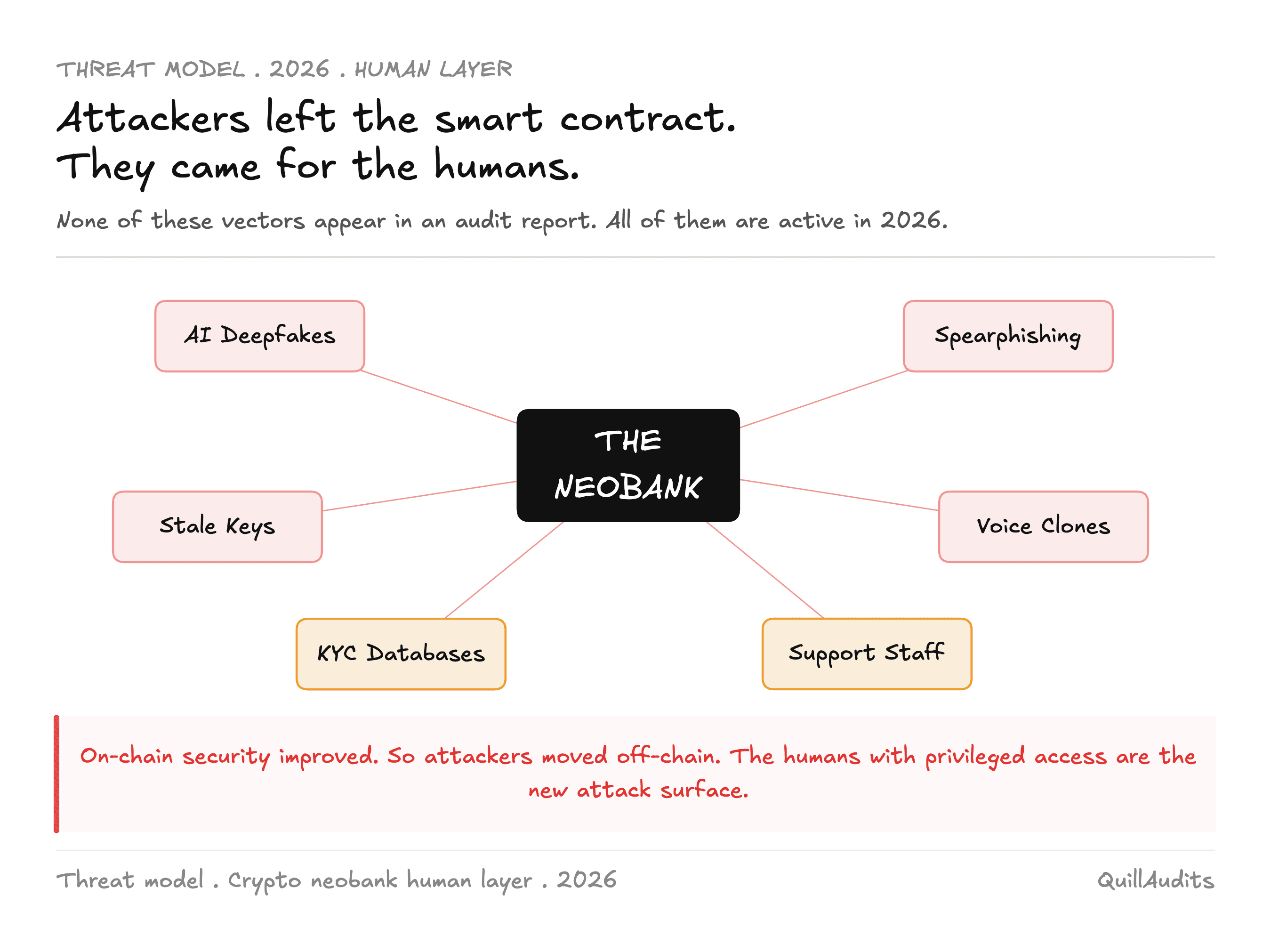

Against this backdrop, the threat environment has also matured. On-chain security has improved. Auditing is more rigorous. Formal verification is becoming more common. So attackers have moved.

The most sophisticated threat actors have shifted substantially toward social engineering and infrastructure compromise. AI-generated deepfakes are being used to impersonate founders in video calls. Voice clones bypass communication verification. Spearphishing campaigns target developers with privileged access by name, using publicly available GitHub and LinkedIn data to craft convincing lures.

For a crypto neobank, the human layer is often the most exposed. Developers with admin key access. Contractors who still hold operator roles. Customer support staff with access to KYC databases. None of these are on-chain. None of them appear in an audit report. All of them are targets.

The custody layer carries the other major concentration of risk. Hot wallet architecture without HSMs, without signing quorums, without key rotation, is a liability that scales directly with TVL. The platforms raising $100M and growing user deposits are simultaneously growing the size of the target on their back. Security posture has to scale with the balance sheet or it becomes the constraint.

What QuillAudits Brings to This Problem

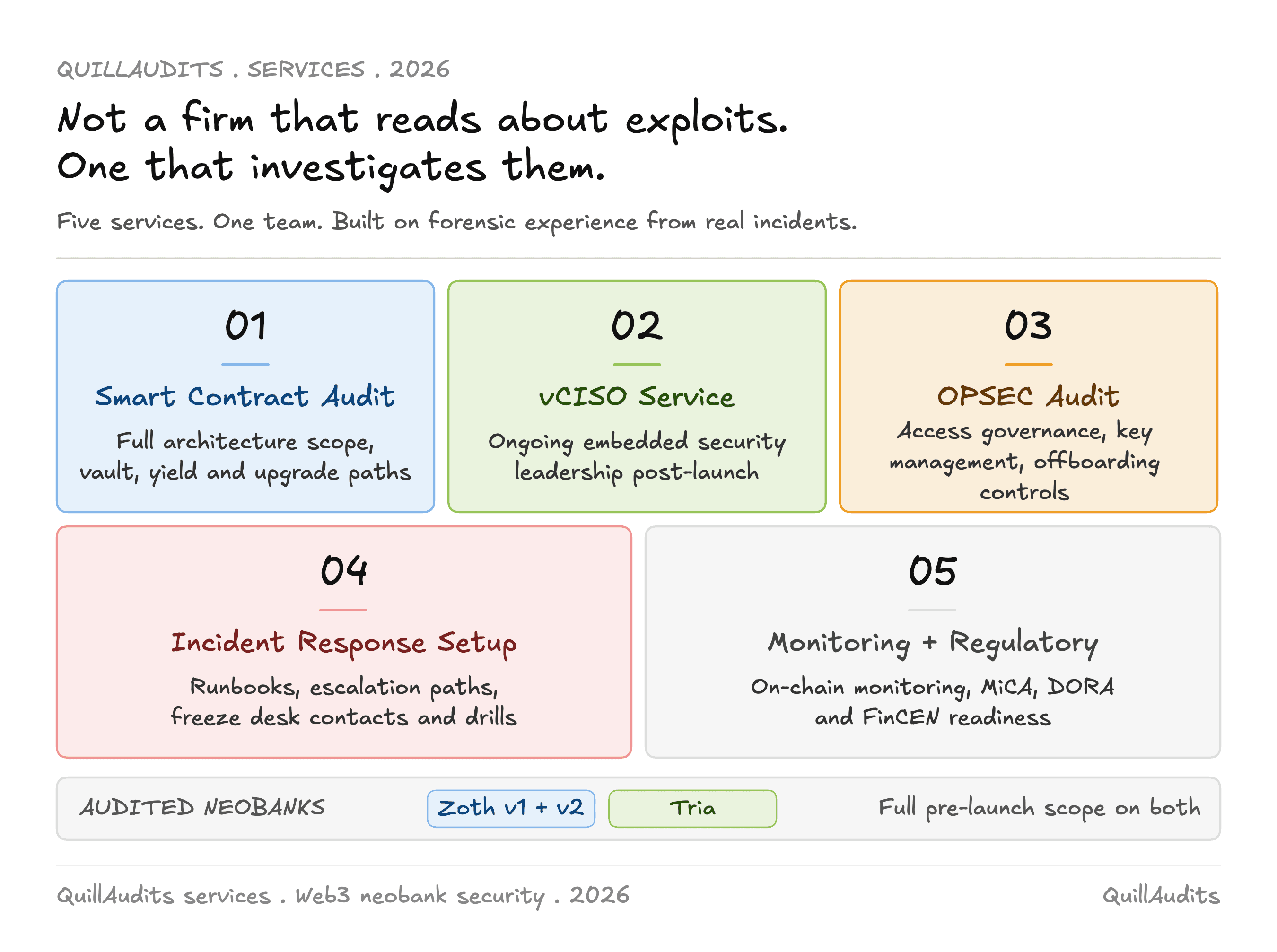

QuillAudits has been on the forensic side of these incidents. That is not a firm describing blockchain security from the outside. It is a team that has investigated real exploits, traced fund flows, identified root causes, and documented the specific failure modes that take platforms in this category down.

That forensic experience is the foundation of how QuillAudits approaches security engagements for crypto neobanks. And it is not theoretical. QuillAudits has audited live, production-stage neobanks that are already in market.

Zoth is building what it describes as the world's first privacy-first stablecoin neobank for retail and institutions, combining neobank accessibility with blockchain transparency, DeFi yield, card payments, and compliance in a single platform. QuillAudits completed two rounds of smart contract auditing for Zoth, covering both v1 and v2 of its protocol architecture. The scope covered the full vault and yield layer, not just the surface contracts.

Tria is a self-custodial global crypto neobank that launched in December 2025 with a debit card available in 150+ countries, letting users spend, trade, and earn from a single balance across all chains without bridges, gas fees, or seed phrases. QuillAudits audited Tria's smart contract infrastructure before its public launch, providing the security foundation for a product that now operates across an unusually broad cross-chain surface.

Both engagements reflect a specific audit philosophy for this product category: the scope has to match the architecture. A neobank is not a token contract. It is vault logic, yield routing, multi-chain state management, card settlement interfaces, and upgrade paths, each one carrying its own risk profile. Auditing only the core contracts and calling it done is the same mistake as auditing only the front door of a building with twelve other entrances.

Smart contract auditing is the starting point. QuillAudits has audited hundreds of protocols across EVM and non-EVM chains, covering the full range of vulnerability classes. For a neobank, that scope extends to the full contract architecture, including vault logic, yield integrations, card settlement contracts, and upgrade mechanisms.

The vCISO service is an ongoing function. The model delivers embedded security leadership at a fraction of the cost of a full-time hire. In practice, that means owning the access governance process, running periodic access reviews, building the incident response runbook, setting security requirements for integration partners, conducting developer security briefings, producing board-level security reporting, and running continuous threat modeling as the product evolves. It is not a retainer for occasional advice. It is the security function, operated externally.

Regulatory readiness is the third layer. For platforms pursuing MiCA authorization or US MSB and MTL compliance, security documentation is not optional. QuillAudits supports the development of the security frameworks, incident reporting procedures, and operational resilience documentation that regulators in both regions are increasingly requiring as part of the authorization process.

Conclusion

The rise of stablecoin-native banking is no longer a prediction; it is already happening. Capital, infrastructure, and regulation are aligning, but growth alone does not create resilience. The platforms that endure will be those that treat security as an ongoing operational discipline rather than a checkbox exercise. Audits provide a snapshot of code quality, but long-term survival depends on continuous security ownership. Funding may accelerate growth, but sustainable financial infrastructure is ultimately built on strong security foundations, not capital alone.

Contents